Print

Print Email

Email

Two new options have been added to Medicare Supplement plans while four have been eliminated. Offerings of some current plans have also changed.

Medicare Supplement insurance (also known as Medigap insurance) is designed to help pay some of the health care costs not covered by Medicare, such as annual co-pays and deductibles. As of June 1, 2010, new laws brought changes to Medigap policies.

How does Medigap insurance work?

Medigap policies are labeled alphabetically (A through N) for ease of comparison and are standardized from state to state and insurance company to insurance company. (Except for Massachusetts, Minnesota and Wisconsin—if you live in one of these states, contact your state insurance company or a private insurer who operates in your state as plans in these states offer different coverage.) Part A is the basic, or core, policy; each plan after adds more and more coverage. Read more about Medigap Supplement insurance.

What has changed with Medigap insurance?

Elimination of four policies. Four plans—E, H, I and J—were eliminated from the Medigap policy offerings. Part E became unnecessary when Medicare added screening procedures for breast, cervical, colorectal and prostate cancer to its coverage and Parts H, I, and J became obsolete once a prescription drug benefit was added to Medicare and at-home recovery benefits, which were underutilized and outdated, were eliminated from Medigap policies altogether.

Addition of two policies.

Parts M and N were added to provide additional choices to supplement Medicare coverage. Part M covers 50 percent of the Part A inpatient hospital deductible (but does not cover the Part B deductible) and fully covers skilled nursing facility daily coinsurance changes. In addition, Part M covers medically necessary emergency care in a foreign country (subject to a $250 deductible).

Part N includes 100 percent coverage of the Part A inpatient hospital deductible (but also does not cover the Part B deductible), skilled nursing facility copayments, and the foreign travel emergency benefit. It also covers Part B coinsurance for covered services of up to $20 for health care provider office visits and up to $50 for emergency room visits.

Hospice coinsurance.

Part A now includes hospice coinsurance as a basic benefit, which includes outpatient prescription drug and inpatient respite care coinsurance. Part K will cover these costs up to 50 percent and Part L will cover these costs up to 75 percent.

Part B coinsurance.

Parts K, L and N now require you to pay a portion of Part B coinsurance. All other policies pay this at 100 percent.

Part B excess charges.

Part G now covers Part B excess charges at 100 percent. Excess charges are health care charges above the amount approved by Medicare.

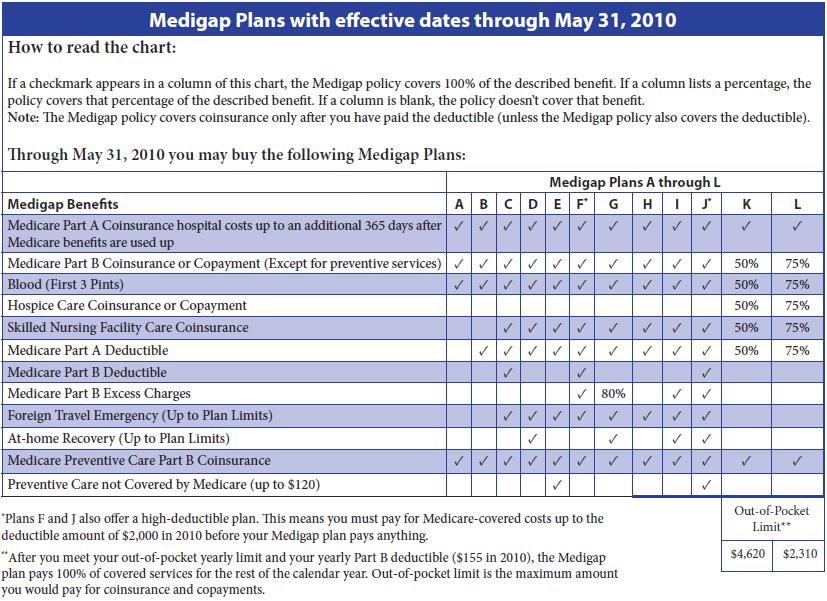

For easy-to-read comparisons, view the Medigap Plans available through May 31, 2010 and the Medigap Plans available on or after June 1, 2010.

How do the Medigap Supplement changes affect you? If you purchased your Medigap plan before June 1, 2010, your plan continues to be guaranteed renewable. This means your plan will automatically renew each year as long as you continue to pay your premiums. (Older policies may become more expensive, however, as the number of policy holders declines.) Those with older policies who wish to switch to the new Medigap policies may replace a policy of equivalent or lesser coverage without being subject to pre-existing condition waiting periods or probationary periods, as long as they maintained coverage for at least six months.

For those new to the Medigap market, the best time to buy a Medigap policy is during your Medigap open enrollment period, which begins the first day of the month (and continues six months thereafter) in which you are 65 years of age or older and enrolled in Medicare Part B. During this period, an insurance company cannot refuse to sell you any Medigap policy it sells, make you wait for coverage or charge you more because of pre-existing conditions.

For help in choosing a Medigap policy that is right for you, check out the guide published by the Centers for Medicare & Medicaid Services, entitled Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.

Related Articles

- Do You Need Medicare Part D Insurance?

- Pick The Medicare Part D Plan That's Right For You!

- Why You Need A Personal Health Record

- Affordable health insurance: How to save on your health-care costs

- Purchasing Individual Health Insurance: What you need to know

- Prescription Insurance

- HMO Insurance

- Do You Need Long Term Care Insurance?

- Why You Need Long Term Disability Insurance

- Medicare Prescription Drug Coverage

- Medigap Supplemental Insurance Explained

- Supplemental Insurance - What Is It?

- Medical Marijuana - Should Marijuana Be a Medical Option?

- Prescription Drugs - Should They Be Advertised to Consumers?

{kind=link}